Stop Late Invoices: AI Payment Collection for Small Business

AI payment collection for small business, explained: what it costs, UK legal limits, and a decision matrix for Xero and QuickBooks users.

The Verdict: AI payment collection for small businesses is software that uses machine learning and conversational AI to chase overdue invoices with minimal human effort — predicting which invoices will go late, drafting reminder sequences, and in some cases handling follow-up calls. For UK SMBs it works best as a pre-legal chasing layer plugged into Xero or QuickBooks, not as a full debt-recovery replacement.

Critical Insights:

- Three distinct categories exist: automated dunning (email/SMS sequencing), predictive prioritisation (ML ranks late-risk invoices), and AI voice agents (phone calls) — each has a different SMB fit profile.

- Realistic SMB pricing runs £30–£200/month for dedicated dunning SaaS; “free” tiers typically cap below 20 invoices/month and omit dispute-flag workflows.

- AI chasers break even once they shave roughly 3–5 debtor days off a book invoicing £20,000+/month — below that threshold, Xero’s built-in reminders are usually cheaper.

- UK compliance has three hard edges: the Late Payment of Commercial Debts (Interest) Act 1998 (statutory 8% + Bank of England base rate plus £40–£100 compensation), GDPR Article 22 (no solely-automated decisions with legal effect), and the FCA perimeter for B2C consumer debt.

- Never let AI automate the letter before action, call consumers without human review, or chase a disputed invoice — all three are customer-relationship or legal landmines.

It’s Sunday evening and you’re drafting chaser emails again. AI payment collection for small business owners promises to take this weekend tax off your plate — but only if you pick the right category and stay the right side of UK law.

Every week you don’t chase costs cashflow. Every week you do chase costs your time, your weekend, and the quiet awkwardness of Monday’s phone call. A collections agency wants 10–30% of what they recover, and a solicitor’s letter before action almost always ends the client relationship for good. This article sits inside our complete guide to AI for small business, which covers the wider automation picture.

What AI Payment Collection Actually Does: The Three Categories

It’s not one product. AI payment collection is three distinct categories which look similar in vendor marketing and behave very differently once connected to your accounting ledger. Know which one you’re buying before you sign anything.

Start with the term the industry uses: dunning. Dunning is the methodical process of communicating with customers to collect money owed — the sequence of reminders, follow-ups and escalations running from the day you send an invoice to the day it’s paid. Most UK SMB owners do this by hand in their inbox. AI payment collection automates the first three-quarters of it.

Category 1: Automated Dunning (Email, SMS, WhatsApp)

Automated dunning tools send scheduled reminder sequences triggered by invoice age. The software watches your accounting ledger, waits for an invoice to hit a defined age (say, day +3 overdue), and sends a pre-drafted message via email, SMS or WhatsApp. More advanced tools personalise tone, rotate subject lines, and suppress sending on weekends or bank holidays.

Representative tools in this category include Chaser, Satago, and the built-in reminder features inside Xero, QuickBooks, FreeAgent and Sage. The “AI” label here is often light — the intelligence sits in the sequencing and the template library, not in any deep machine learning. That isn’t a bad thing: for most SMBs this category delivers the best return.

Category 2: Predictive Prioritisation

Predictive prioritisation adds a machine-learning layer ranking outstanding invoices by their probability of going late. The model typically learns from a rolling 6–12 months of your ledger history — which customers pay on time, which drift by days, which industries take 45+ days as a matter of course — and produces a daily priority queue so your chasing effort lands on the invoices most at risk.

Examples include Upflow and the AR insights features built into FreshBooks and larger finance platforms. This category becomes useful once you have enough ledger volume for the model to learn — typically 50+ invoices a month, mixed across reliable and unreliable customers.

Category 3: AI Voice Agents

AI voice agents are conversational AI systems placing or answering collection phone calls. The agent reads from an LLM-driven script, handles common customer responses (promises to pay, disputes, “not my account”), and hands off to a human when the conversation leaves its comfort zone.

This is the highest-risk category for customer relationships and the tightest fit for UK compliance. A voice agent mis-handling a dispute, calling a consumer, or mistaking a reconciled payment for a non-payment will cost you the client and their referrals for good. Use voice only on known B2B contacts, low average invoice value, and high volume.

What AI Does Not Do

AI payment collection is a pre-legal chasing layer. It doesn’t replace solicitors, it doesn’t draft letters before action to the standard a court will accept, and it doesn’t file county court claims. If an invoice is genuinely bad debt — 90+ days overdue, no response, clear refusal — AI tooling won’t recover it. That work still runs through human drafting and regulated legal process.

How AI Predicts Which Invoices Will Go Late

It learns the patterns humans notice inconsistently. AI compares each new invoice against the signals which historically preceded late payment, assigns a risk score, and triggers an earlier or softer intervention before the due date passes.

The signals the better models actually use are unglamorous: customer payment history (the most predictive single feature), invoice value against that customer’s norm (a £12,000 invoice to someone who usually gets £2,000 ones is more likely to drift), day-of-month sent, customer industry, and time since last contact. Nothing exotic — just features a human credit controller would weigh by instinct, applied consistently across every invoice on the ledger.

The biggest leverage sits in pre-empting lateness, not chasing it. A polite, tonally-soft nudge three days before the due date — “just flagging invoice #1043 is due Friday, anything you need from us?” — costs nothing and reliably prevents a meaningful chunk of late payments. Research and anecdotal SMB case studies put the reduction at roughly 30% of would-be late invoices, though your mileage depends heavily on your customer mix.

The pre-due-date sequence most tools will let you configure looks like this:

- Day -3: soft reminder, friendly tone, includes payment link.

- Day 0 (due date): confirmation message — “due today, reply if anything’s needed.”

- Day +3: polite follow-up, slightly firmer.

- Day +7: escalation, direct ask, invoice copy attached.

- Day +14: formal notice — this is where human review must take over.

Human judgement still has to sit in the loop at three points. First, tone: no AI reliably reads the difference between a cashflow-strapped long-term client and a new customer testing how firm you are. Second, relationship flags: VIP clients and retainer relationships should sit on an allowlist pausing automation. Third, disputes: any reply mentioning “dispute”, “query”, “wrong”, “already paid” or “not agreed” must pause the sequence and route to you.

Is AI Payment Collection Right For Your Business?

Three questions decide it. If you answer yes to all three, dedicated AI dunning will probably pay for itself. Fail any one and you should start somewhere cheaper.

- Do you send 20+ invoices a month? Below this volume, the subscription cost outruns the time saved.

- Are your debtor days above 30? If you’re already paid in 25 days, there’s very little room for AI to improve things.

- Are your customers predominantly B2B? B2C chasing falls inside the FCA perimeter and most SMB-grade AI tools aren’t built or authorised for it.

Who should NOT bother yet: businesses sending fewer than 20 invoices a month (use Xero or QuickBooks built-in reminders — they’re included in your subscription), mostly-B2C businesses (FCA risk outweighs time saved), and high-trust professional services like law firms, accountancy practices and boutique consultancies where aggressive auto-tone can silently damage retention.

Quick cost/benefit framing before the full matrix below: if your monthly invoicing sits under about £20,000 and your debtor days are under 30, the honest answer is “not yet — tighten terms first.” If you invoice £40,000+ a month with debtor days of 40+, almost any competent dunning tool will pay for itself inside a quarter.

The Decision Matrix: Which Approach Fits Your Business

Self-triage in under 60 seconds. Find the row best matching your profile, then read across for the recommended category, realistic cost band, the single compliance flag you must not ignore, and a sensible pilot path.

| Your profile | Recommended category | Typical monthly cost (GBP) | Key compliance flag | Pilot approach (first 30 days) |

|---|---|---|---|---|

| Under 20 invoices/month, B2B, average value < £2,000, Xero or QuickBooks user | Built-in accounting reminders (Xero invoice reminders, QuickBooks automated statements) | £0 (included in existing subscription) | None beyond standard T&Cs | Enable reminders at +1, +7, +14 days. Review replies weekly. Reassess after 60 days. |

| 20–150 invoices/month, B2B, average value £500–£20,000, debtor days > 30 | Dedicated AI dunning SaaS (email/SMS sequencing with tone controls) | £30–£200 | GDPR Art. 22 — keep a human-approval toggle on any message with legal consequence | Connect accounting sync, import overdue ledger, run automated emails only (no SMS) with human approval for anything past 30 days overdue. |

| 50+ invoices/month, mixed ageing buckets, want to know which invoices to chase first | Predictive prioritisation (ML risk-ranking layered on dunning) | £80–£400 | Data residency — confirm UK/EU hosting before syncing ledger | Feed 6–12 months of historical invoice/payment data. Run model in shadow mode for 30 days before acting on scores. |

| 200+ invoices/month, B2B, low-to-mid invoice value, tolerant of automated voice contact | AI voice agent (layered on top of email/SMS dunning) | £200–£800 + per-call charges | Call recording consent + FCA perimeter check if any customer is a consumer | Voice agent handles only the +14 day reminder call to known B2B contacts. All first contact and all escalations stay human. |

| Any volume, B2C or regulated consumer credit exposure | Do NOT use SMB-grade AI collection tools. Stick to built-in reminders plus human review. | n/a | FCA CONC rules apply — most SMB AI tools are not authorised | Talk to an FCA-authorised collections partner before automating anything. |

| High-trust professional services (legal, accounting, consultancy), any volume | Dedicated dunning SaaS with full human-in-the-loop, tone set to "soft" | £30–£150 | Reputation risk — auto-send is off by default; every message is human-reviewed | Draft-only mode for 30 days. You approve every send. Measure reply sentiment before loosening. |

| Fewer than 10 overdue invoices in a typical month | None. Manual chasing in your accounting tool is cheaper than any subscription. | £0 | None | Reassess in 6 months or if overdue volume doubles. |

What It Costs — And When It Pays For Itself

Four pricing tiers. Built-in accounting reminders cost nothing beyond your existing Xero/QuickBooks subscription. Dedicated AI dunning SaaS runs £30–£200/month for a business sending 20–150 invoices. Predictive prioritisation platforms charge £100–£500/month and need a meaningful ledger history to be worth it. AI voice agents are usage-based: expect £1–£5 per completed call on top of a platform fee.

Use this arithmetic to sanity-check whether an AI chaser will actually pay for itself. No vendor benchmarks, just pure maths.

Inputs: M = Your monthly invoicing (GBP) D = Days of DSO you realistically expect to shave off R = Your blended cost of capital or overdraft rate (annual %) S = Annual subscription cost of the AI tool (GBP) H = Hours/month you currently spend chasing W = Your hourly opportunity cost (GBP)

Monthly cashflow value of recovered days: CashValue = (M * D / 30) * (R / 12)

Monthly time value recovered (AI removes ~60% of chasing hours): TimeValue = H * 0.6 * W

Monthly subscription cost: ToolCost = S / 12

Net monthly benefit: Net = CashValue + TimeValue - ToolCost

If Net > 0 the tool pays for itself. If Net < 0 stick with built-in reminders.

Worked example — a typical UK SMB: M = £40,000/month invoicing; D = 4 days DSO improvement; R = 9% overdraft rate; S = £1,200/year; H = 6 hours/month chasing; W = £45/hour.

- CashValue = (40,000 × 4 / 30) × (0.09 / 12) = £40/month

- TimeValue = 6 × 0.6 × 45 = £162/month

- ToolCost = £100/month

- Net = +£102/month. The tool pays for itself, but mostly on time saved, not on cashflow.

Three interpretation rules. If your Net is positive but driven only by TimeValue, a cheaper tool — or better use of built-in reminders — may beat a paid SaaS. If CashValue alone covers ToolCost, the case is strong: the tool pays back in cashflow terms before you count your own time. If Net is negative, don’t subscribe. Tighten payment terms, invoice faster, or lean on your accounting tool’s built-in reminders.

UK Legal Ground You Must Not Skip

Most SERP content skims the legal side. That’s a mistake, because three UK rules change what “AI collection” is actually allowed to do.

The Late Payment of Commercial Debts (Interest) Act 1998 gives you statutory rights against late-paying business customers. You can claim interest at 8% above the Bank of England base rate plus a fixed compensation fee of £40–£100 per invoice (scaled by invoice value). Most AI collection tools do NOT automatically claim this — you have to invoke the Act explicitly on the invoice or in the demand. If a vendor tells you their product “automatically claims statutory interest,” read the small print carefully; in most cases the product just templates the language for you to sign off.

GDPR Article 22 restricts solely-automated decisions producing legal effects on a person. A fully autonomous AI sending a formal letter before action to a sole trader or consumer falls squarely inside Article 22. The Information Commissioner’s Office can fine, and — more importantly for cashflow — your customer can formally object and pause your collection process indefinitely. Practical implication: the final formal notice and anything legal-stage must have a human in the loop. An AI draft a human reads and approves is fine. An AI send with no human review is not.

The FCA perimeter and CONC rules apply to consumer debt. If any of your customers are individuals (not businesses), and especially if the debt is regulated consumer credit, you’re operating inside a regulated space. Most SMB AI collection tools are built for B2B and aren’t authorised for consumer debt collection. Using them against consumers can breach CONC rules even if you didn’t realise the customer counted as a consumer. If your ledger is mixed B2B/B2C, either segment consumer debts out of any AI workflow or route them via an FCA-authorised collections partner.

One more check before you sign any contract: data residency and sub-processors. Your customer ledger is personal data. Confirm in writing the vendor hosts data in the UK or EU and list the sub-processors they share data with. If they can’t answer in one email, that tells you something.

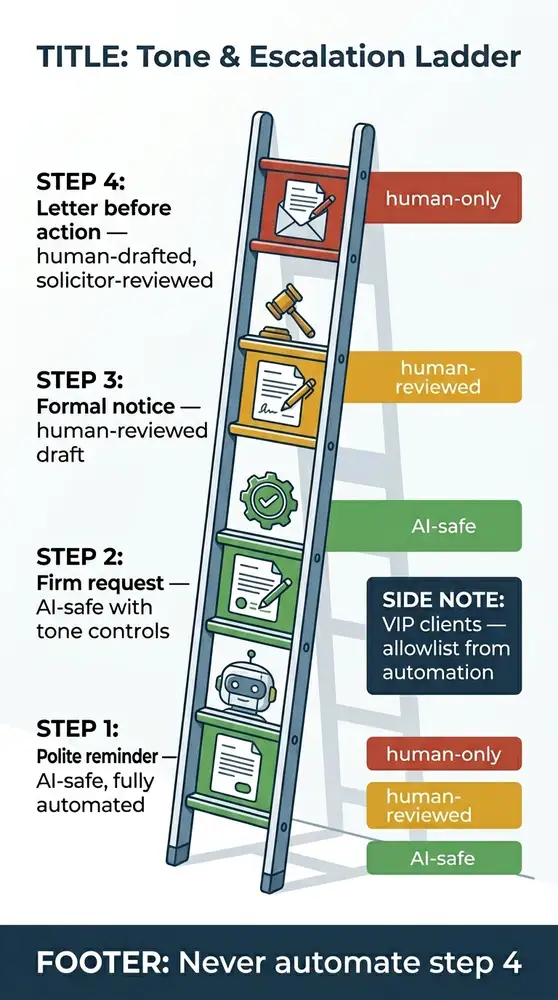

The Tone & Escalation Ladder: Keeping Customers You Still Want

The biggest unspoken fear about AI chasers is they’ll sound aggressive and cost you clients. It’s a legitimate worry. The fix is a four-step escalation ladder with clear rules about which steps AI owns and which a human owns.

- Step 1 — Polite reminder. Tone: warm, assumes best intent. AI-safe, fully automated. Template example: “Just a quick reminder that invoice #1043 is due Friday — let me know if anything’s needed our end.”

- Step 2 — Firm request. Tone: direct, still courteous. AI-safe with tone controls enabled. Used at +3 to +7 days overdue. “Invoice #1043 is now 5 days overdue. Could you confirm a payment date this week?”

- Step 3 — Formal notice. Tone: businesslike, references terms. Human-reviewed draft — AI writes it, you read it before it sends. Used at +14 days.

- Step 4 — Letter before action. Tone: formal, cites the Late Payment Act, warns of county court claim. Human-drafted or solicitor-reviewed. Never automated.

Two configuration rules make the ladder work in practice. First, set up a VIP client allowlist — any customer you particularly care about retaining bypasses automation entirely and goes straight to your manual review queue. Second, turn on dispute-flag pausing so any customer reply containing words like “dispute”, “query”, “wrong”, “not agreed” or “already paid” automatically pauses the sequence and routes to a human. This is a non-negotiable feature: if a tool doesn’t have it, don’t buy it.

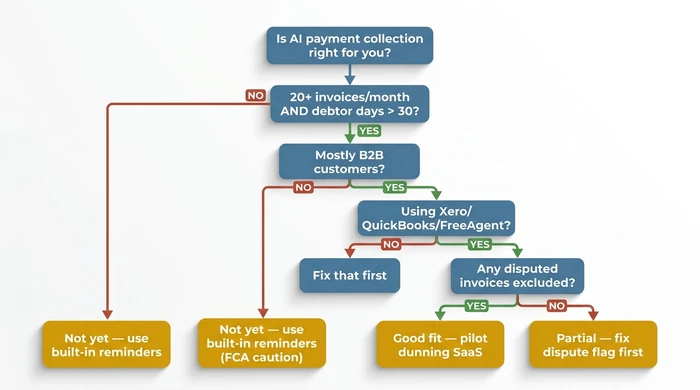

Visual Decision Tree: Is AI Payment Collection Right For You?

Work down the table row by row. Stop at the first row matching your situation and follow the action.

| Scenario | Action | Reasoning |

|---|---|---|

| Fewer than 5 overdue invoices per month AND debtor days under 30 | Do not subscribe to an AI tool yet. Turn on built-in reminders in Xero/QuickBooks. | Problem is too small to justify subscription cost. Manual chasing plus native reminders is cheaper and faster to deploy. |

| 5+ overdue invoices/month, debtor days over 30, customers are businesses (B2B), cloud accounting in place | Pilot a dedicated AI dunning SaaS with human-in-the-loop enabled. | This is the core SMB fit profile. B2B reduces FCA risk; cloud accounting makes sync feasible; volume justifies £30–£200/month. |

| Customers are consumers (B2C) or regulated consumer credit | Stop. Do not use SMB-grade AI collection tools. Use only built-in reminders and consider an FCA-authorised partner. | FCA CONC rules apply to consumer debt collection. Most SMB AI tools are not authorised; misuse risks regulatory breach and customer harm. |

| No cloud accounting tool in use (spreadsheets or paper) | Fix that first. Migrate to Xero, QuickBooks, FreeAgent, or Sage before evaluating AI tools. | Every SMB-grade AI collection tool requires an accounting sync. Without it, you are paying for manual data entry. |

| B2B, volume justifies tooling, but customers are high-trust professional relationships | Use dunning SaaS in draft-only mode: AI drafts, you approve every send for the first 30 days. | Aggressive auto-tone damages retention in relationship-driven sectors. Human review protects goodwill while you learn the tool's voice. |

| Any invoice is disputed or under query | Flag the invoice to pause all automation. Handle the dispute manually until resolved. | AI chasing a disputed invoice escalates complaints and can trigger GDPR Art. 22 objections. Dispute-flag pause is a non-negotiable tool feature. |

| Invoice is 60+ days overdue and you're preparing a Letter Before Action | Take AI out of the loop. Human-draft or solicitor-review the LBA. | LBAs have legal consequence. GDPR Art. 22 restricts solely-automated decisions with legal effect; county courts expect human authorship. |

| B2B, 200+ invoices/month, low average value, tolerant of voice automation | Layer an AI voice agent on top of existing email/SMS dunning — B2B known-contacts only. | Voice economics only work at volume with low relationship-damage risk. Keep consumer contact and escalations off voice entirely. |

| Vendor quotes £500+/month and you send under 50 invoices/month | Walk away. Choose a tier-appropriate tool or stay on built-in reminders. | Enterprise pricing cannot break even at SMB invoice volumes. You would pay more in subscription than you recover in faster cash. |

Warnings: Don’t Let AI Send the Legal Stuff

The Common Mistake: Owners set an AI dunning tool to “fully autonomous” and let it run the whole ladder — from first polite nudge to letter before action and threats of county court claim. Vendors encourage this, because “end-to-end automation” sells better than “AI drafts, you approve.”

Why it’s dangerous — three concrete risks, in rising order of cost:

- GDPR Article 22 breach. UK GDPR restricts solely-automated decisions producing legal effects on a person. An AI-generated letter before action to a sole trader or consumer falls squarely in scope. The ICO can fine, and your customer can formally object and pause your collection indefinitely.

- FCA perimeter breach if any customer is a consumer or regulated consumer-credit counterparty. Most SMB AI tools are not FCA-authorised. Automated chasing of a consumer can breach CONC rules even if you didn’t realise the customer counted as a consumer.

- Reputation damage that outlasts the debt. An AI voice agent misreading a dispute, or sending a “final notice” to a client whose payment hadn’t reconciled, costs you the client and their referrals for good. You recover £2,000 and lose £20,000 of lifetime value.

The expert alternative: Run AI on steps 1 and 2 only — the polite reminder and firm request. Hard stop at the “formal notice” stage: a human reviews every message, and the letter before action is drafted or reviewed by you or a solicitor. Turn on dispute-flag pausing so any reply containing “dispute”, “query”, “wrong”, “not agreed” or “already paid” auto-pauses automation. Keep AI voice agents off B2C entirely. Human-in-the-loop is the default, not the upgrade.

Red flags when evaluating vendors:

- Demos showing an AI agent sending a “letter before action” or “final demand” without a human approval step.

- Tools without an explicit dispute-flag / pause trigger in the workflow builder.

- “Autonomous collections” marketing with no mention of GDPR Art. 22 or FCA CONC.

- Pricing tiers that gate the human-approval toggle behind a higher plan.

- No UK/EU data residency option.

- Claims that the AI will “automatically claim statutory interest under the Late Payment Act” — most don’t, and the claim must be explicitly invoked.

How To Pilot AI Payment Collection in 30 Days

Four weeks. One real decision at the end: expand, adjust, or cancel.

- Week 1 — baseline. Export your last 90 days of invoices from Xero/QuickBooks. Calculate current debtor days and identify the 10–20 most persistently late customers. Note the hours per week you currently spend chasing. Without this baseline, you can’t measure anything.

- Week 2 — set up. Pick one category (start with dunning if unsure — it’s the safest bet for most SMBs). Connect the tool to your accounting software, import contacts, configure tone settings to “soft” or “neutral”, enable the dispute-flag pause, and put your VIP clients on an allowlist.

- Week 3 — narrow pilot. Run AI against one segment only: for example, invoices aged 3–30 days overdue from non-VIP B2B customers. Keep manual chasing on everything else. Watch replies daily for the first three days, then every other day.

- Week 4 — decide. Measure three things: change in debtor days, complaints or tone-related replies, and hours saved. If debtor days dropped by 3+ and no complaints landed, expand cautiously. If debtor days moved but complaints rose, adjust tone and re-pilot. If nothing moved, cancel — you’ll have a clean answer for the next vendor pitch.

Variations and Exceptions

- Your customers are consumers (B2C). Most SMB-grade AI tools are not suitable. FCA rules apply. Use manual reminders or a regulated collections provider.

- You send fewer than 20 invoices a month. Dedicated AI tools will not pay back. Use Xero/QuickBooks built-in automated reminders — they are free and surprisingly capable.

- You run a high-trust professional service (law, accountancy, consulting, retainer agency). Disable voice automation entirely. Set the first step to human-approval and leave it there for at least 90 days.

- You invoice international customers. Check GDPR cross-border transfer rules and language fit. English-only AI voice agents will not land well with EU debtors.

- An invoice is disputed. Manually flag and exclude before any AI sequence runs. No exceptions, no “just this once.”

- The debt is genuinely bad (90+ days, unresponsive customer, clear refusal). AI will not recover it. Move to solicitor LBA or county court claim via the Money Claim Online service.

FAQ

Q: Is AI invoice chasing legal in the UK?

Yes — for B2B pre-legal chasing under the Late Payment of Commercial Debts (Interest) Act 1998 and GDPR Article 22, provided a human reviews any legal-stage message. B2C chasing is FCA-regulated and most SMB AI tools are not authorised for it. If your customers are businesses, you’re clear; if they’re consumers, stop and take advice.

Q: Will customers know it’s AI?

Yes, and most won’t mind for routine reminders. Customers care about tone and timing, not the “AI” label. A polite reminder arriving at 9am on a Tuesday is welcome whoever wrote it; an aggressive one at 11pm on a Sunday is not. Get the tone and timing right and the author barely matters.

Q: How much can AI realistically cut debtor days?

Credible UK SMB case studies report reductions of 5–15 days inside 90 days of deployment. Anything more depends on where you started: if your debtor days are 60+, the gains are larger; if you’re already at 25, there’s little room to improve. Assume 5 days for budgeting purposes and treat anything above that as upside.

Q: Does it work with Xero and QuickBooks?

Yes — any credible SMB tool syncs with both, plus FreeAgent and Sage. Reject any tool which doesn’t. Ledger sync isn’t a feature, it’s the baseline; without it you’re just paying for manual data entry dressed up as automation.

Q: Can AI claim statutory late-payment interest for me?

No, not automatically in most cases. You generally need to invoke the Late Payment of Commercial Debts Act explicitly in your invoice terms and your demand letter. Some tools template the language for you — helpful — but the legal act of claiming still requires a human to sign off and send.

Q: What’s the smallest business that benefits?

Roughly 20+ invoices a month and £20,000+ in monthly invoicing. Below that, Xero or QuickBooks built-in reminders will usually win on cost, and your time is better spent tightening payment terms and invoicing faster than onboarding a new SaaS tool.

Conclusion: The Honest Summary

AI payment collection is a pre-legal chasing layer, not a debt-recovery replacement. The SMB fit filter is simple: enough volume to justify a subscription, predominantly B2B customers, cloud accounting already in place, and disciplined handling of disputed invoices. Start with the decision matrix above, pilot one category for 30 days, and keep a human in the loop on anything with legal weight.

If your business clears the fit filter, a £30–£200/month dunning tool is likely the single highest-ROI piece of finance automation you can deploy this year. If it doesn’t, fix the fundamentals first — tighter payment terms, faster invoicing, Xero’s built-in reminders — and revisit in six months. For the wider picture on automating other parts of your operation, read our complete guide to AI for small business.

Founder, Too Many Hats

Free tool

What it's costing you

See how many hours your manual tasks are really costing you.

Free tool

Problem Solver

Describe your biggest timewaster and get a personalised plan.

Related Guides

AI Sales Follow Up: Stop Ghosting Your Warm Leads

AI sales follow up for founder-sellers: score leads, fire triggers, draft the first touch, and call the right lead today — without burning your domain.

AI Customer Service for Small Business: 3 Modes, 30-Day Path

AI customer service for a small business in three modes — deflection, routing, AI assist — plus the handover seam that protects quality. 30-day path.

How to Reduce Errors in Business Processes (Forensic Guide)

Reduce errors in repetitive business processes with a three-lever sequence: redesign, automate, protect. Scorecard, worked example, 5 rights pattern.